Home

>

Blog

>

>

12 Questions Underwriters Should Ask Before Trusting an APS Summary

An APS summary should reduce underwriting uncertainty, not hide it. These twelve questions help underwriters evaluate whether the summary is complete, traceable, and useful for risk review.

An APS summary should make medical evidence easier to review. It should not ask the underwriter to blindly trust that everything important was captured. A strong summary organizes, condenses, cross-references, and flags documented information so the underwriter can review the applicant's medical history with better visibility.

Before relying on an APS summary, underwriters should ask these twelve questions.

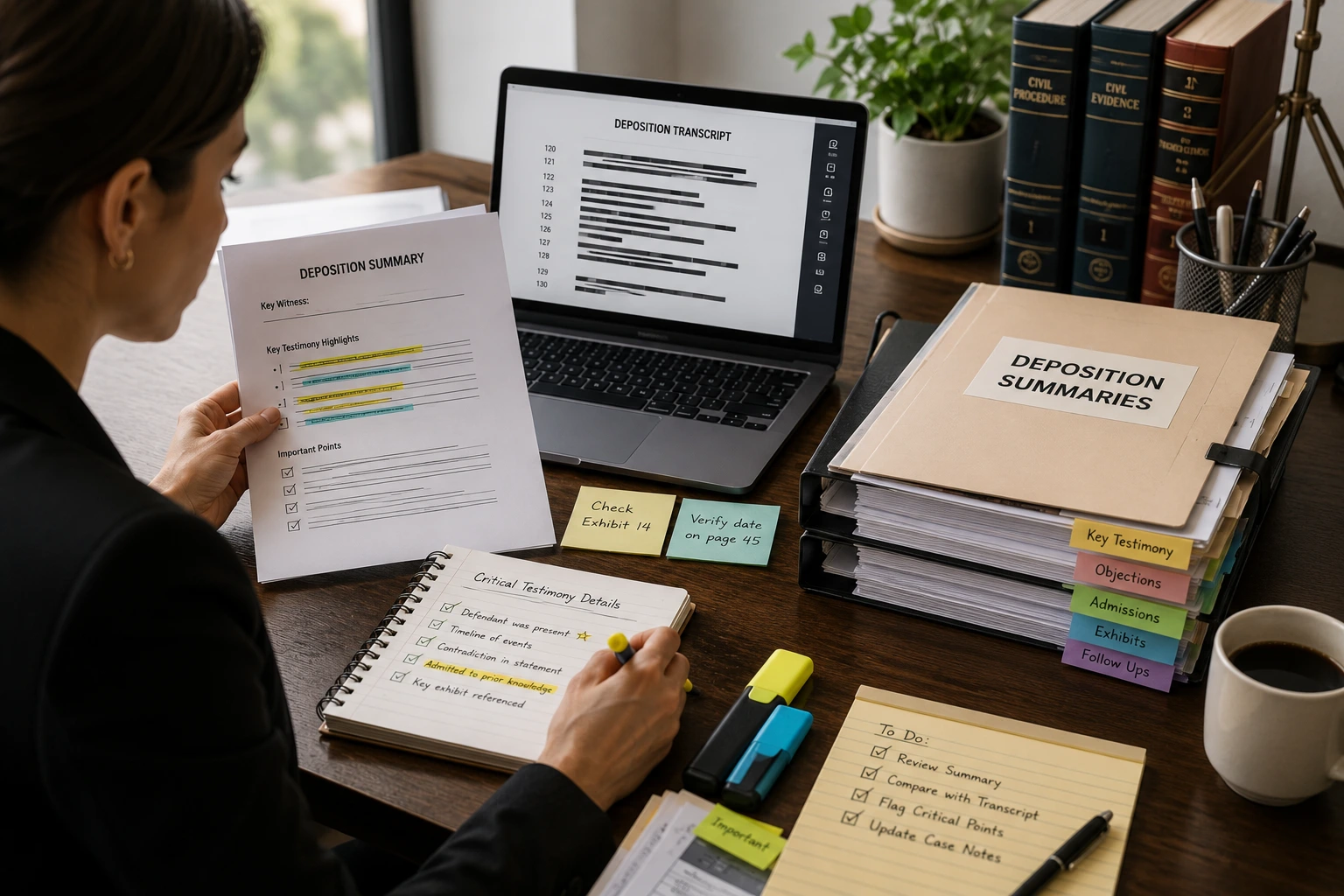

1. Does the summary identify the full record scope?

A useful APS summary should make the source material clear. The underwriter should know what records were reviewed, which providers were included, and what date range the summary covers.

If the original APS includes records from a cardiologist, primary care provider, endocrinologist, hospital, and pharmacy file, the summary should not treat the material as one generic medical history. It should show the underwriter where the information came from.

1. Provider names

The summary should identify the major sources of medical information.

2. Record date ranges

The underwriter should know whether the summary covers two visits or several years of treatment.

3. Document types

Office notes, labs, imaging, discharge summaries, and medication lists should be distinguishable.

Without scope clarity, the underwriter may not know whether the summary reflects the full APS or only a portion of it.

2. Are diagnoses and medical conditions tied to documented sources?

A diagnosis listed without context can create confusion. The summary should show where the diagnosis appears and whether it was documented as active, historical, suspected, ruled out, or monitored.

For example, a condition appearing in a past medical history list may not carry the same context as a condition discussed in a recent specialist assessment. The summary does not need to interpret the underwriting significance of that difference, but it should preserve the documented context.

The underwriter should ask whether the summary connects diagnoses to:

- Provider notes.

- Dates of service.

- Specialist assessments.

- Hospital or emergency records.

- Lab or imaging support when available.

24 to 48 Hours for Indexing

Once records are received, sorting and indexing can be completed within 24 to 48 hours so the APS summary team works from an organized record set.

3. Does the summary include current and historical medications?

Medication history can reveal important clinical context. It may show active treatment, discontinued therapy, dosage changes, medication adherence issues, or conditions not clearly discussed elsewhere in the record.

An APS summary should not simply list a few medications from the most recent note if the record contains years of medication changes. It should help the underwriter see patterns and relevant updates.

Ask whether the summary captures:

1. Current medications

Especially those tied to chronic or monitored conditions.

2. Significant medication changes

Starts, stops, dosage changes, or new specialist-prescribed drugs.

3. Medication indications when documented

The summary should not guess why a medication was prescribed, but it can include the stated reason when the record provides it.

4. Adherence notes when documented

Missed doses, stopped medications, or intolerance may appear in provider notes.

4. Are lab values, imaging findings, and test results summarized with context?

Underwriters often fear missing objective medical details buried in the APS. Labs, imaging reports, cardiac testing, pulmonary studies, pathology reports, or procedure findings may be scattered across the record.

A strong APS summary should not drown the underwriter in every normal value. It should surface relevant abnormal findings, follow-up recommendations, and notable trends when documented.

The summary should answer:

- What tests were performed?

- When were they performed?

- What findings were documented?

- Were follow-up tests recommended?

- Were results reviewed by a provider?

The reviewer should summarize documented findings without creating a diagnosis or interpreting risk beyond the record.

5. Does the summary flag gaps or missing records?

Silence can be misleading. If the APS appears to skip from one year to another, or if a provider references a hospital admission that is not included, the summary should flag that gap.

Missing information matters because the underwriter may otherwise assume the record is complete. A good summary helps identify where the record itself may be limited.

Useful gap notes include:

- Referenced specialist records not included.

- Missing hospital discharge summaries.

- Lab results mentioned but not attached.

- Imaging ordered but report absent.

- Follow-up visit recommended but not found in the provided record.

Want to see what a fully traceable APS summary looks like before you rely on one?

6. Are chronic conditions followed across time?

Many APS records include chronic conditions that appear repeatedly across multiple provider visits. A summary should help the underwriter see how those documented conditions were monitored over time.

This is especially important for records involving diabetes, hypertension, cardiac disease, pulmonary conditions, kidney disease, cancer history, psychiatric treatment, or neurological conditions.

The summary should show:

1. First documented mention in the provided record.

2. Ongoing treatment or monitoring.

3. Specialist involvement when present.

4. Medication or treatment changes.

5. Relevant labs or diagnostic follow-up when included.

The purpose is not to classify risk. The purpose is to organize the medical story so the underwriter can apply the carrier's guidelines with clearer evidence.

7. Does the summary separate active issues from past history?

A past condition listed in a medical history section can create fear if it is not clearly separated from current treatment. Underwriters need to see whether a condition is being actively treated, monitored, resolved, historical, or simply listed without discussion.

The APS summary should preserve that distinction when the record supports it.

For example:

1. A remote surgery should not be blended with a recent hospitalization.

2. A historical diagnosis should not be presented as a current active complaint unless the record shows it.

3. A ruled-out condition should not be summarized as confirmed.

4. A screening recommendation should not be treated as a completed diagnosis.

This is where human review matters. The reviewer must read the context around the term, not just extract the term.

"A trustworthy APS summary should make the original medical evidence easier to verify, not harder to trace."

8. Are hospitalizations, surgeries, and procedures easy to find?

Hospital records and procedure reports often carry high-value context for underwriting review. They may explain why the applicant was admitted, what procedure was performed, what findings were documented, and what follow-up was recommended.

The summary should make these events easy to locate.

Ask whether it captures:

- Admission and discharge dates.

- Reason for hospitalization when documented.

- Procedure name and date.

- Operative or pathology findings when included.

- Discharge diagnoses and follow-up plans.

If the APS references a procedure but the report itself is missing, that should be flagged.

9. Does the summary show follow-up recommendations and compliance notes?

A provider's plan may be just as important as the visit itself. Follow-up recommendations can show what the treating physician wanted to monitor, repeat, refer, or rule out.

A useful APS summary should include documented follow-up plans such as:

1. Repeat labs.

2. Specialist referrals.

3. Imaging follow-up.

4. Medication review.

5. Lifestyle or monitoring instructions.

6. Return visit intervals.

If the record later shows that follow-up was completed, the summary should connect those pieces. If the follow-up is recommended but not found in the provided record, that limitation should be visible.

10. Can the underwriter trace key statements back to the record?

Trust depends on traceability. If an APS summary says a diagnosis, test result, hospitalization, or provider recommendation exists, the underwriter should be able to locate the source record.

Traceability may come through page references, Bates numbers, provider/date citations, or source file names. The format can vary, but the principle is the same: important statements should not float without support.

What Underwriters Should Expect From APS Summaries

75%

Of Trust Issues Trace Back to Missing Source Links

A summary that can't point back to a page or Bates number is one you can't verify.

60%

Of Weak Summaries Blend Active and Historical Findings

Without clear separation, a resolved condition can read like an active one.

90%

Of Reliable Summaries Are Human-Reviewed, Not Just AI-Extracted

Context, like what's missing or ruled out, is what automated extraction alone tends to miss.

11. Does the summary avoid unsupported interpretation?

An APS summary should not overstep. It should not decide whether a condition changes underwriting classification. It should not infer causation, predict outcomes, or provide medical advice.

The strongest summaries stay disciplined. They summarize what the record documents, flag what appears missing or unclear, and preserve context for the underwriter.

Watch for risky language such as:

- Claims that a condition is harmless without source support.

- Statements that a risk is resolved without provider documentation.

- Assumptions about why a medication was prescribed.

- Conclusions that belong to underwriting guidelines, not the summary writer.

A reliable summary helps the underwriter think clearly. It does not think on behalf of the underwriter.

12. Was the APS summary reviewed by a trained human reviewer?

AI-assisted tools can support document sorting, extraction, and organization. But APS summaries need human review because medical records are full of context.

A trained reviewer can notice when a diagnosis appears only in a history list, when a lab trend needs to be grouped, when a follow-up is mentioned but absent, or when two providers document the same issue differently.

Human review helps protect the summary from becoming a simple extraction sheet. It keeps the focus on organized, review-ready medical evidence.

To wrap up,

Underwriters do not fear APS length alone. They fear the hidden detail: the missed diagnosis, the unflagged follow-up, the buried hospitalization, the medication change that never made it into the summary.

A trustworthy APS summary reduces that fear by making the medical record clearer, traceable, and easier to review. These twelve questions help underwriters decide whether the summary in front of them supports careful risk review or still leaves too much uncertainty behind.

Source Credit : All metrics derived from LezDo TechMed’s internal project data.

Vishnu Priya Vinu

Vishnu Priya Vinu is a Medical-Legal Research Analyst with over two years of experience in medical record review, medico-legal research, and content development. She specializes in blogs, articles and E-books that bridges the gap between healthcare and law. Her strong medical background brings depth and accuracy to content, enabling law firms, medical evaluators, and insurance professionals to gain insights on complex medical data analysis. She delivers evidence-based insights and strategic content that strengthen case outcomes and support informed decision-making.