Home

>

Blog

>

>

The Most Overlooked Details in APS Summaries: Why They Matter?

Small omissions in APS summaries can lead to major underwriting errors. Capturing every detail is essential for accurate risk assessment.

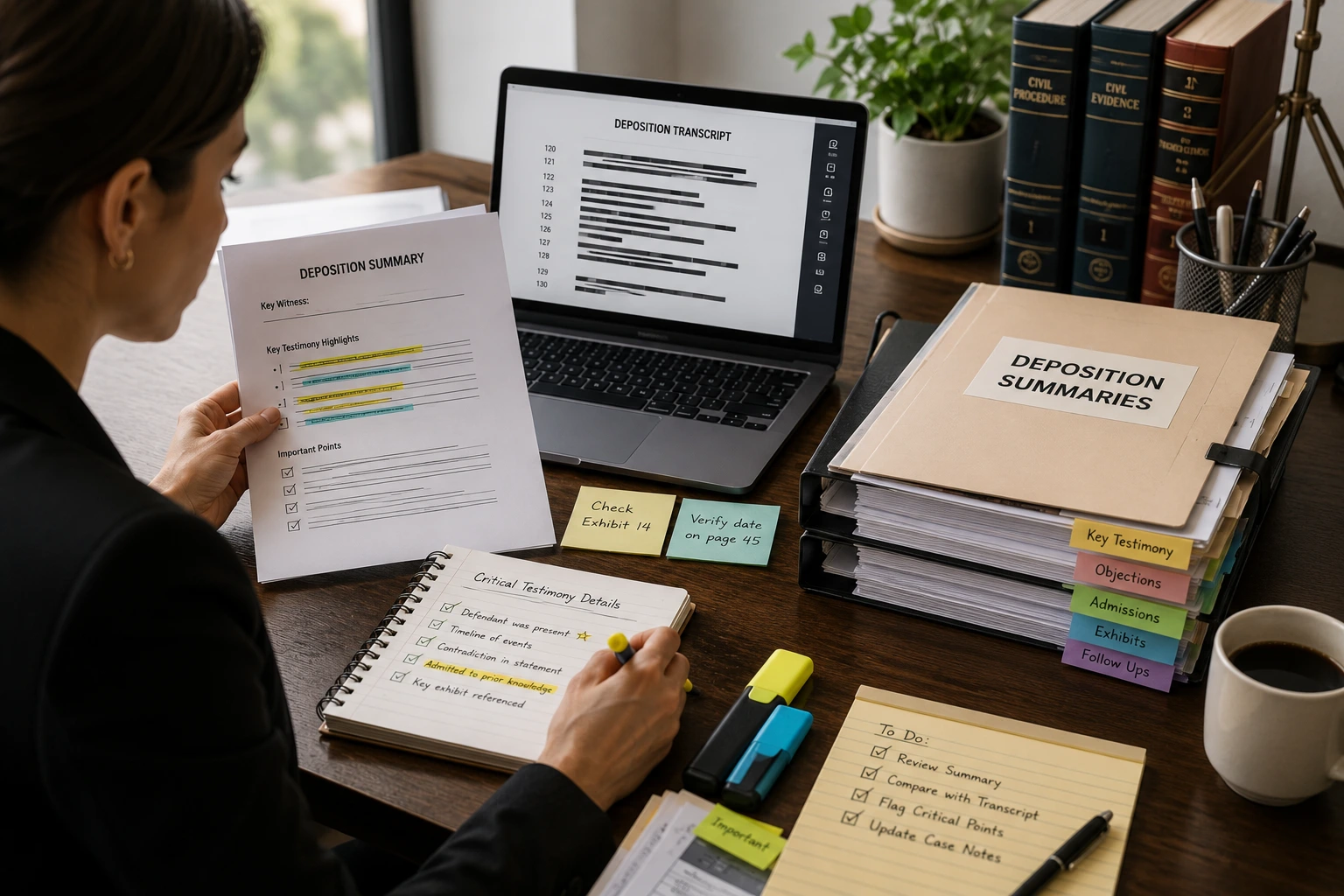

In insurance underwriting, Attending Physician Statements (APS) are essential documents that contain valuable evidence of an applicant's medical history, which gives underwriters the ability to assess risk accurately. APS summaries are aimed at obtaining clinical information and displaying them in a user-friendly way. Although very often, crucial information is not incorporated; these omissions may have a negative effect on underwriting, claims processing, and even risk assessment of the entire insurance company.

This blog will discuss the most commonly overlooked details from APS summaries, and why they are important to insurance providers.

15–25% Accuracy Boost

Including functional, medication, and mental health details in APS summaries improves underwriting precision and reduces disputes.

Common Gaps in APS Summaries and Their Impact on Risk Assessment

- Incomplete Chronology in APS Summaries

One of the most common errors in APS summaries is the omission of a clear and chronologically formatted timeline of medical events. Physicians and healthcare professionals usually document events in chronological order as they occur. When APS summaries fail to show the connection between symptoms, diagnoses, treatments, and outcomes, it compromises the clarity and accuracy of APS summary.

Why It Matters

- Incomplete chronologies can flatten the progression of chronic illnesses.

- Can lead to an underestimation of the severity or recurrence of a chronic condition.

- Chronology is an important factor in determining recovery, prognosis, and future claims.

Tip for Providers

Ensure summaries include date-stamped entries for diagnoses, hospitalizations, surgeries, and follow-up dates, providing an overall medical narrative.

- Missing Functional Status and Lifestyle Impact

APS reports may contain lifestyle factors such as smoking, alcohol consumption, diet, and exercise, that directly affect risk assessment but tend to be poorly summarized or often left off completely. APS summary reports tend to focus on clinical data, including lab results, medications, and diagnostics. They often overlook functional status (the ability to work, mobility, and cognitive function). Functional status is the crucial piece of information that demonstrates how a condition will impact daily life and overall risk.

Why It Matters

- Functional limitations can have a direct effect on disability claims and long-term care needs.

- Lifestyle impact distinguishes between controlled and uncontrolled conditions.

- It provides context to underwriting decisions beyond the information contained within the medical data.

Tip for Providers

Include notes that discuss work restrictions, physical limitations, and mental health status included in the summary to provide an additional perspective on the patient's health status.

Check Our APS Summary Samples

- Incomplete Reporting of Family Medical History

Even though APS summaries focus on the applicant's medical history, entries about the applicant's family medical history are also important and should not be ignored. The reviewers may skip the family medical history if the physician just briefly refers to it, such as, "father died of heart disease at the age of 55."

Neglecting this information removes some of the important family history regarding heritability, especially cardiology, oncology, and metabolic conditions.

Why It Matters

- Family medical history gives us some predictive insights by indicating inherited predispositions that may not yet be shown in the applicant’s own medical history.

- Lack of Context Around Medications

Medication lists are standard in APS summaries, but they often lack context, such as the reason for the prescription, whether the medication is ongoing, and how the patient has responded to it.

Why It Matters

- Some medications may suggest serious underlying reasons not even considered.

- Changes in dosages may indicate improvement or deterioration.

- Having multiple prescriptions may indicate a more complex health concern that may require more focused review.

Tip for Providers

Annotate medication lists with indications, beginning and end dates, and treatment outcomes.

- Missing Mental Health Indicators

Mental health is frequently underrepresented in APS summaries, particularly if there is a primary concern for physical health. But mental health conditions can significantly affect mortality, morbidity, and insurability.

Why It Matters

- Depression, anxiety, and cognitive disorders could impact compliance with treatment.

- Mental health issues can create additional risks in a disability insurance or life insurance policy.

- Early signs (e.g., sleep disturbances, behavioral changes) are often buried in notes.

Tip for Providers

Document a psychiatric assessment, therapy notes, or even simple behavioral observations. Don’t hesitate to include even minor details.

- Unclear or Missing Diagnostic Rationales

Some APS reports refer to diagnoses but do not highlight how a provider arrived at the diagnosis. It may be unclear as to how a diagnosis is made, whether it was made from imaging, laboratory reports, or purely clinical observations, which carries a risk of misinterpretation.

Why It Matters

- Diagnostic accuracy affects underwriting risk classification.

- Misunderstood diagnoses can lead to unnecessary exclusions or premium hikes.

- Clear rationale supports transparency and defensibility in claims.

Tip for Providers

Provide a short description or reference to the evidence to support the diagnosis, even for the major conditions.

- Failure to Attend to Social Determinants of Health

Social determinants, including housing, employment, family support, and substance use, are often omitted from documentation or rarely included. However, it affects health outcomes considerably.

Why It Matters

- Social factors shape the experience of recovery, following treatment recommendations, and long-term prognosis.

- Social determinants provide context for high-risk behavior or environmental exposure.

- The lack of documentation can result in an incomplete risk assessment.

Tip for Providers

Wherever available, include social history such as family, education, and relevant lifestyle factors such as daily diet, exercise, and sleep.

“Overlooked APS details affect risk assessment. Structured reviews bring clarity through complete documentation.”

How Insurance Companies Can Enhance APS Summaries

Keep these mistakes in mind and focus on three key enhancements.

- Structured Review Frameworks

Use standardized templates that force reviewers to document context, treatment progress, and lifestyle factors in detail.

- Medical Language Training

Make sure the reviewer and underwriters know how to accurately interpret medical terminology, including abbreviations and shorthand.

- Quality Audits and AI Assistance

Quality audits on a regular basis, combined with AI-driven summarization tools to enhance the detection of missing information, inconsistencies, and data points, improve overall efficiency.

Optimizing APS Summary Reviews

28%

Accuracy Boost

Detailed summaries improve underwriting accuracy

22%

Contextual Clarity

Lifestyle and mental health data strengthen underwriting

35%

Efficiency Gains

AI tools improve speed and consistency

APS Summaries & Underwriting Accuracy

What is an APS summary in insurance underwriting?

An APS (Attending Physician Statement) summary is a condensed, structured overview of an applicant’s medical history, created from physician records to help underwriters assess risk accurately and efficiently.

Why are APS summaries so critical for underwriting decisions?

APS summaries directly influence risk classification, premium pricing, exclusions, and approvals. Even small omissions can lead to misjudged risk, claim disputes, or financial loss.

What are the most commonly missed details in APS summaries?

Key gaps often include incomplete medical timelines, missing functional status, lack of medication context, overlooked mental health indicators, and absent social or lifestyle factors.

How does an incomplete medical chronology affect underwriting?

Without a clear timeline, underwriters may miss disease progression, recurrence patterns, or recovery gaps—leading to underestimation or overestimation of long-term risk.

Why is functional status important in APS summaries?

Functional status shows how a condition impacts daily life, work ability, and independence. This information is essential for disability, long-term care, and life insurance risk evaluation.

Do lifestyle factors really impact underwriting outcomes?

Yes. Smoking, alcohol use, diet, exercise, and compliance with treatment significantly affect morbidity and mortality risk, making them vital for accurate underwriting decisions.

Why should medication context be included, not just medication lists?

Medication purpose, duration, dosage changes, and response reveal disease severity and stability. A simple list without context can hide serious underlying conditions.

How do mental health details influence insurance risk assessment?

Mental health conditions can affect treatment compliance, recovery outcomes, and long-term insurability. Early indicators are often subtle but highly relevant to underwriting accuracy.

What role do social determinants of health play in APS reviews?

Social factors like employment, housing stability, family support, and substance use influence health outcomes and long-term risk, providing essential context beyond clinical data.

How can insurance companies improve APS summary quality?

By using structured review templates, trained medical reviewers, quality audits, and AI-assisted tools to identify missing data, inconsistencies, and overlooked risk indicators.

To wrap up,

APS summaries are not simply medical outlines; they are an essential element for ensuring thorough underwriting. The absence of an aspect like the applicant's health history timeline, lifestyle factors, or medication details can lead to risk classification and affect claim outcomes.

By ensuring clarity, consistency, and context, along with using structured reviews and AI tools, insurance providers can turn APS summaries into clear, reliable, and insight-driven assets. In underwriting, even the smallest detail has the power to change the entire picture.

Source Credit : All metrics derived from LezDo TechMed’s internal project data.

Vishnu Priya Vinu

Vishnu Priya Vinu is a Medical-Legal Research Analyst with over two years of experience in medical record review, medico-legal research, and content development. She specializes in blogs, articles and E-books that bridges the gap between healthcare and law. Her strong medical background brings depth and accuracy to content, enabling law firms, medical evaluators, and insurance professionals to gain insights on complex medical data analysis. She delivers evidence-based insights and strategic content that strengthen case outcomes and support informed decision-making.